ERISA Record Retention Requirements In Plain English

ERISA record retention requirements. Say that five times fast.

All joking aside, this is actually pretty serious business. The Employee Retirement Income Security Act of 1974 requires that you retain important plan documentation. Failing to do so can get you into really hot water in the event of an audit.

Despite that, there’s no reason to panic (and we’re definitely still going to make jokes). Abiding by ERISA record retention requirements is all about being responsible and staying prepared.

Here’s what you need know to tackle the ERISA record retention requirements:

Why Record Retention is So Important

The IRS and DoL aren’t just forcing their love of paperwork on you willy-nilly. ERISA requires you to retain plan documents and employee benefit plan information for a few good reasons:

Being Ready for Audits

This is the main reason for retaining plan documents. Audits require a ton of documentation to prove the plan has been responsibly managed and kept in compliance. Most of the documents you’re required to retain are those that you’ll need to supply for an audit.

Sticking to the “Prudent Person” Rule

This is a general rule which requires that the plan administrator go about their duties solely in the interest of the plan participants and with the “care, skill, prudence, and diligence of a prudent person under similar circumstances.”

Basically: no acting like a maniac if you are in charge of someone’s money. You have to manage it conscientiously.

Keeping Plan Administration Stress-Free

A solid record retention policy allows you to quickly and easily respond to employee documentation requests or changes, deal with audits, and keep things compliant. These are all essential aspects of managing employee retirement plans and benefit entitlements.

ERISA Record Retention Requirements

Under Section 107 of ERISA, anyone responsible for filing plan reports must “maintain records to provide sufficient detail to verify, explain, clarify and check for accuracy and completeness.”

Similarly, under Section 209, employers should maintain employee records “sufficient to determine the benefits due or which may become due to such employees.”

So exactly what records and documents are you required to keep?

The 401(k)-Related Records You Need To Keep:

1. Fiduciary Plan Documents

- The original (signed) 401(k) plan document

- 401(k) adoption agreement

- 401(k) plan amendments

- IRS determination letter

- ERISA fidelity bond

- Investment policy statement

- Trust records/Investment statements

2. Contracts & Agreements

- Plan Services Agreement

- Annuity contracts and collective bargaining agreements

- Plan sponsor fee disclosure

3. Participant Notices

- 401(k) summary plan description

- 401(k) summary annual reports

- Blackout notices

- QDIA notices

- Participant fee disclosures

- Participant introduction packets

- Proof that the notices were sent. We also recommend having timestamped logs showing when they were sent, and whether or not they were delivered.

4. Compliance

- Form 5500

- Audited Financial Statements - if your plan was subject to a large plan audit.

5. Participant-Level Benefit Determinations

- Employee demographic information

- Employee offer letters

- Proof of compensation

- 401(k) census data

- Payroll records

- Participant account statements detailing contributions, earnings, loans, withdrawals, etc.

- Participant election forms including:

- Distribution forms (with spousal consent waivers, if applicable)

- Loan documents

- Deferral amount and allocation election forms

- Beneficiary terms

How Long You’re Required to Retain Plan Records

ERISA Section 107 requires that for fiduciary plan documents, contracts & agreements, participant notices, and compliance documents, you are required to keep records for “at least six years from the date the report was filed.”

Participant-level benefit determinations are slightly different. These you have to keep “until the [plan] has paid all benefits and enough time has passed that the plan won’t be audited.”

This can be a while…

Here’s what a well-respected ERISA attorney has to say about holding onto plan records:

"There’s a common misperception that the 6 year rule applies to all records, not just reports and certifications. The biggest problem I see is the failure to keep records long enough. So my advice to plan sponsors? When in doubt, keep it. Keep a written records retention policy, and always consult your ERISA counsel before destroying any plan records."

-Carol Buckmann, Founding Partner, Cohen & Buckmann

Record Storage Rules

Thankfully, the government hates physical paperwork as much as the rest of us.

Nowadays, you can dispose of your physical copies once you’ve made and securely stored electronic copies (if allowed by your state).

However, there are requirements for correct electronic reporting. Your system must ensure:

- Electronic records are safe, secure, manageable, and properly ordered.

- Electronic copies are easily converted to paper.

- Controls are in place to make sure information is reliable, authentic and accurate.

- Records are legible and viewable on a screen format.

- No ERISA reporting and disclosure requirements are violated in the operation of the system.

That’s it for rules, but there are still have some record-management guidelines we would seriously recommend. Here are...

Tips For Keeping Your Documents In Order

1. Go Electronic

It’s way easier to search a computer folder for a document than to go digging through a filing cabinet. And you get fewer paper cuts.

Don’t just take it from us though:

"Most plan sponsors would say the hardest part of the 401(k) audit is accumulating the documentation needed from various people inside and outside their organization. That’s why we recommend electronic storage. Having all 401(k)-related documentation organized in one easy-to-reach place can save plan sponsors a tremendous amount of time."

-Kristine Boerboom, Senior Manager, Wegner CPAs

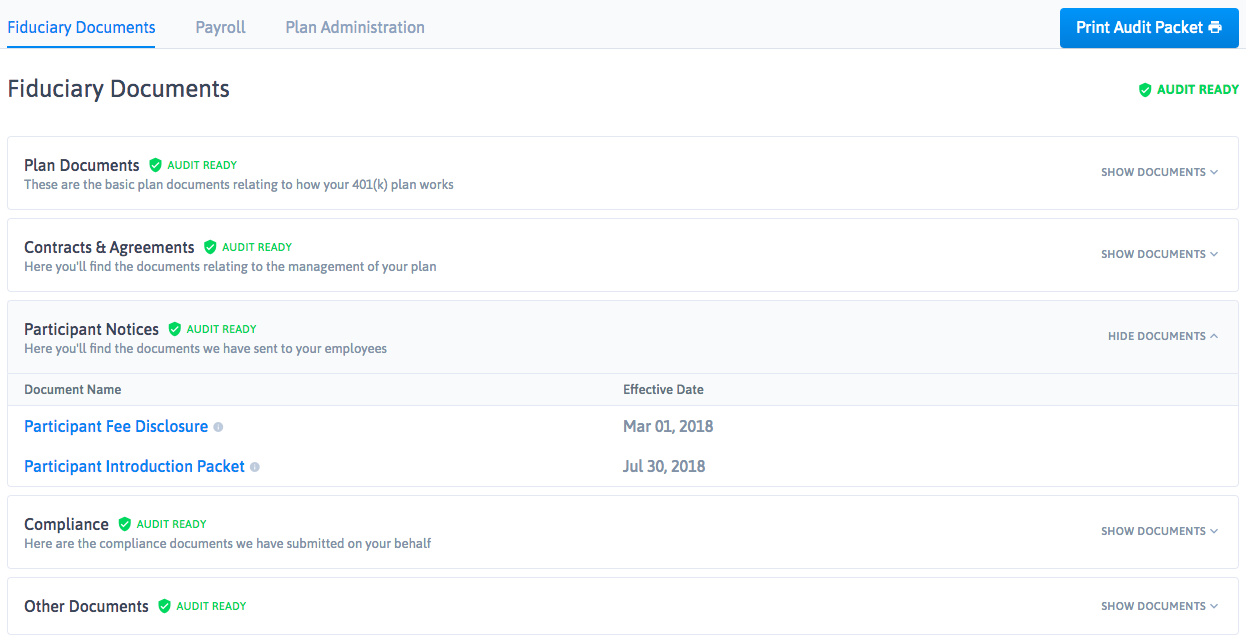

At ForUsAll, we store plan documentation with our Fiduciary Vault - a place to keep all your required documents safe, secure, and always accessible.

Here’s an example:

When the auditors come knocking, rather than running around and digging through files and hard drives and wondering if maybe you threw them out, all you have to do is click that ‘Print Audit Packet’ button and you’re all set!

2. Retro-active Reorganization

If you haven’t been super neat in the past or inherited a less-than-ideal documentation situation from your last plan administrator, this is going to be a pain - but must be done.

Still, it’s a pretty simple process. Dig through and organize your plan documents - taking particular care with the security and accuracy of the files, as mistakes in the organization can be messy to deal with in the middle of an audit.

3. Have Someone Help You

There is no shame in asking for help. Retirement plan service providers can be lifesavers. With 3(16) fiduciary services, ForUsAll can help guide you through the process of moving your records online, setting up easier plan administration, and preparing for (or dealing with) an audit.

Conclusion

And there you have it: the ERISA record retention requirements broken down into plain English.

If you haven’t fallen asleep yet, we’ll close by emphasizing one point...

Maintaining thorough, well-organized records is one of the best things you can do to make 401(k) administration easier. In particular, good document retention gives you the best shot at waking up from the bureaucratic nightmares that are 401(k) audits with your sanity intact.

Mostly intact, anyway.

If you’d like to see a good example of 401(k) document retention done right, schedule a quick, 10 minute demo today to learn how our automated 401(k) solution can save you time and keep you audit ready.